It is hard to believe that 2019 has less than 10 trading days remaining for investors looking to rebalance portfolios prior to year-end.

Looking back at 2019, data center operators faced a plethora of technology and business trends, including: a slowdown in US hyperscale bookings, a spike in hype around multicloud and hybrid IT as enterprise architectures (supported partially by increased availability of secure public cloud on-ramps), growing adoption of software-defined networks for interconnection, expansion of Network-as-a-Service offerings, higher rack power densities driven by high-performance computing and machine learning, "data gravity" driving deployments closer hyperscale compute and storage nodes, "zero-trust” cybersecurity architecture, new subsea cables, edge-to-core initiatives, etc.

However, when it comes to notable events and trends impacting publicly traded data center providers, understanding why 2019 was a banner year for returns would be number-one, followed by blockbuster M&A deals, emergence of a dedicated digital infrastructure-focused ETF, and significant joint ventures (JVs) inked with infrastructure and sovereign wealth funds.

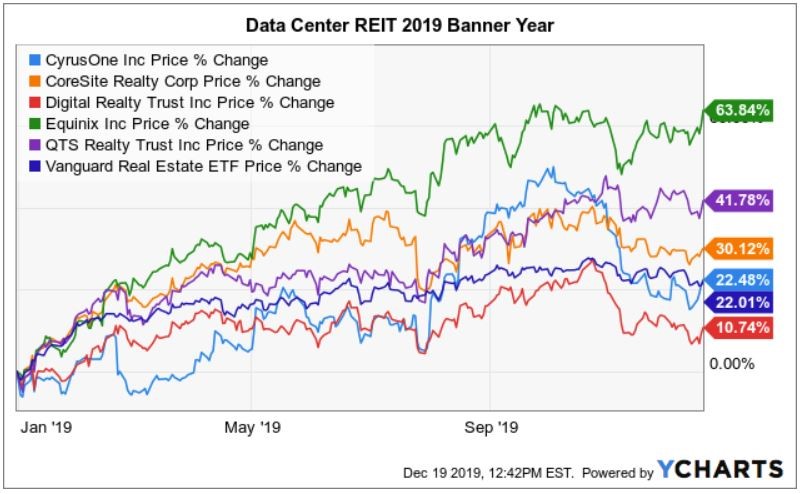

A Banner Year for Returns

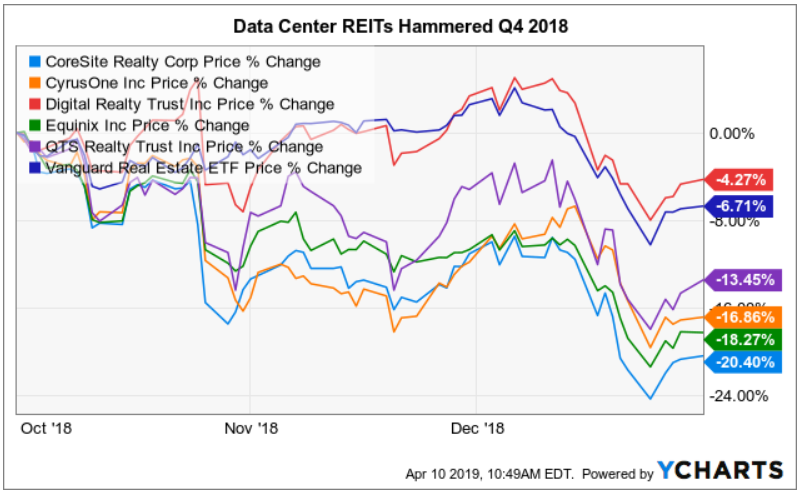

The fourth quarter has seen a "melt up" in US equities, with the S&P 500, DOW 30, and Nasdaq all trading at or near all-time highs. This is in stark contrast with the Q4 2018 meltdown in global equity valuations, which wiped out most gains for the year – and hitting the REIT sector, including data centers, particularly hard.

The brutal selloff last year was likely responsible for about half the good fortune enjoyed by data center REIT shareholders in 2019.

Equinix is an outlier, at the top of the chart, delivering over 60 percent price appreciation. Notably, Equinix shares were severely beaten down at the end of last year, trading in the $335-$350 range. In October, the company reported solid Q3 2019 results, and its global interconnection moat continues to grow, as it layers more products and services onto its software-defined ECX Fabric.

As of this writing, the current Equinix share price is $577 (trading at 23.3x its estimated 2020 AFFO per share), with the analyst-consensus 12-month price objective of $614 per share. Investors seem willing to pay up for the FactSet consensus AFFO growth of nine percent in 2020 and 10 percent in 2021.

Ironically, the relative strength of Digital Realty Trust shares at the end of 2018 resulted in sector-lagging performance in 2019. Digital shareholders were not exposed to gut-wrenching double-digit price declines during the carnage at the end of last year. In fact, Digital was less volatile than Vanguard Real Estate ETF (VNQ), which invests across all REIT sub-sectors.

M&A Blockbusters

Brookfield Infrastructure Partners kicked the year off with its $1.1 billion acquisition of AT&T’s data center portfolio. The deal closed first week of January. Along with announcing close of the transaction, Brookfield launched a new company, called Evoque Data Center Solutions, which provides colocation services out of the 31 data centers in the portfolio.

In May, Zayo Group Holdings announced a definitive merger agreement to be acquired by affiliates of Digital Colony Partners and the EQT Infrastructure IV fund for $35 per share, valuing Zayo at $14.3 billion, including the assumption of $5.9 billion of Zayo’s net debt obligations. Digital Colony is a communications infrastructure-focused investment firm formed as a partnership between Tom Barrack’s Colony Capital and Marc Ganzi’s Digital Bridge Holdings.

On October 29, Digital Realty was the first data center REIT to report Q3 2019 earnings. Along with releasing third-quarter results, the company’s CEO, Bill Stein, announced the “definitive agreement to combine with Interxion,” a leading data center provider in EMEA.

The $8.4 billion merger is anticipated to close in 2020 after receiving regulatory and shareholder approvals.

A Data-Focused ETF for Retail Investors

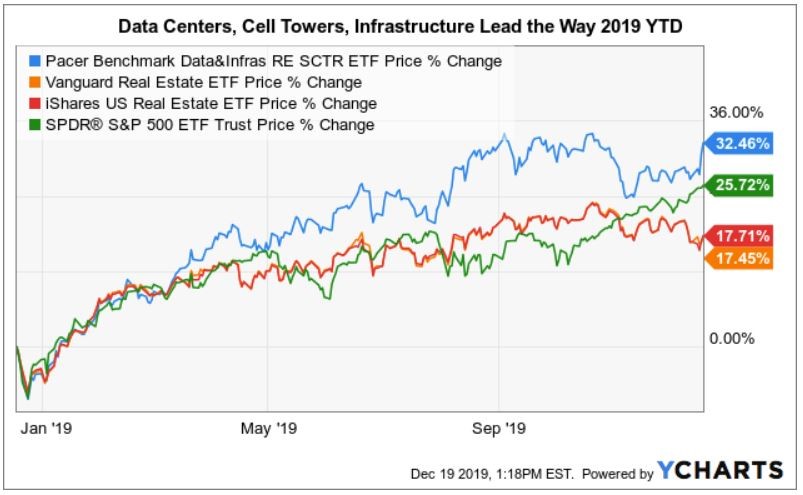

The Pacer Benchmark Data & Infrastructure Real Estate SCTR ETF (SRVR) began trading in May 2018. While it has a long name, SRVR (think "server") simplifies investing in a basket of real estate equities focused on the growth of big data, AI, IoT, and future 5G infrastructure, and related applications.

Notably, technology REITs, including data centers, wireless towers, and related infrastructure, have led the way in 2019, outperforming two broad real estate sector ETFs, as well as the red-hot S&P 500 ETF (currently trading a record highs).

According to the SRVR ETF fact sheet, there are 18 holdings, including the five US-based data center REITs, along with the Chinese wholesale data center giant GDS Holdings, Interxion, and the US colocation heavyweight Switch. The ETF's top five holdings are: Equinix at 15.3 percent, American Tower at 14.2 percent, Crown Castle at 14.2 percent, GDS at 5.7 percent, and Lamar Advertising at 5.1 percent.

The SRVR ETF tracks a rules-based index licensed from Benchmark Investments. This index is rebalanced quarterly to ensure that no constituent company exceeds 15 percent, and the top five holdings do not exceed 50 percent of the index valuation.

Traditional real estate sub-sectors like office, retail, and apartments typically struggle to maintain occupancy when unemployment rises and consumer spending contracts. Owning a basket of real estate/technology companies might outperform more traditional real estate sectors if the global economy slides into a recession. However, it can be challenging for an average retail investor to own a portfolio of individual equities. The basket of data and infrastructure names the SRVR ETF tracks could be an alternative.

Note: This is not investment advice. Always perform your own due diligence and consult with your investment and tax professionals prior to making decisions regarding any investment.

Infrastructure Investors Fund Data Center JVs

Developing data centers is a capital-intensive undertaking, even for multi-billion-dollar-market-cap operators with access to publicly traded equity and debt.

One way to meet the challenge of funding increasingly large hyperscale data center requirements while maintaining a strong balance sheet has been creating a joint venture with an institutional investor, private equity, or a sovereign wealth fund.

These joint ventures often involve project level financing, allowing a public company to utilize a greater percentage of debt to drive higher returns. In addition, "off-balance-sheet" JVs usually include management fees for the data center operators, which also increase returns on invested capital.

This trend continued during 2019 with several notable transactions:

QTS

In February, QTS Realty announced a joint venture with Alinda Capital Partners, selling half of a massive facility it’s building for a single cloud company in Manassas, Virginia, to the infrastructure fund. Alinda is paying $53 million for its half of the joint venture with QTS, but this is only the beginning. The investor appears ready to put as much as $500 million in various hyperscale data center projects with the developer over the next five years.

Equinix

In early July, Equinix announced that it will form a $1 billion joint venture with GIC, Singapore's sovereign wealth fund. The partnership will focus on building across Europe’s four primary data center markets, collectively referred to as FLAP: Frankfurt, London, Amsterdam, and Paris.

The brand for data centers operated under the JV – owned 80 percent by GIC and 20 percent by Equinix – will be xScale. It’s a new name for the initiative and for the team behind it, which used to be called the Hyperscale Infrastructure Team, or HIT. Six European xScale sites are planned so far, with about 155MW of data center capacity total. Notably, Equinix’s xScale strategy isn’t limited to the JV with GIC, or to the European market.

Digital Realty

In April, Digital Realty announced closing of its joint venture with Brookfield Infrastructure, an affiliate of Brookfield Asset Management, one of the largest owners and operators of infrastructure assets globally. Brookfield acquired approximately 49 percent of the total equity interest in the JV, which owns and operates Ascenty, the leading data center provider in Brazil.

MC Digital Realty is a 50/50 joint venture between Mitsubishi Corporation and Digital Realty formed in 2017. In June, Digital Realty announced the completion of the JV's second Osaka data center anchored by a leading global cloud service provider. The four-story facility is reinforced with seismic isolation systems, spans over 23,000 square meters, and will deliver up to 28MW of total IT capacity.

In September, Digital Realty announced an additional land purchase in Tokyo. The new site is strategically located in Greater Tokyo's Inzai data center cluster, in close proximity to the five-acre parcel MC Digital Realty acquired earlier this year, likewise located in the Inzai data center cluster and expected to support development of a 38MW facility (NRT10). The two parcels will be combined to construct a connected campus, expected to deliver more than 120MW of total IT capacity for global and regional customers.

Digital Realty also announced definitive agreements with affiliates of Mapletree Investments Pte Ltd and Mapletree Industrial Trust for the sale of a portfolio of 10 Powered Base Building data centers and the establishment of an 80/20 joint venture on three existing Turn-Key Flex hyperscale data centers in Ashburn, Virginia. The total consideration for both transactions will be approximately $1.4 billion.

GDS

Shanghai -based GDS Holdings recently formed a 90/10 joint venture with GIC, the Singapore sovereign wealth fund, to finance build-to-suit solutions at existing hyperscale customer campuses in remote areas.

This approach allows GDS to assist with facility requirements for its largest customers while maintaining focus on its primary-market strategy (with minimal impact to the balance sheet). GDS is in the process of developing a dedicated team to support this initiative.

Looking Ahead

In 2020, I expect "edge-to-core" initiatives to support smart cities, 5G/IoT, manufacturing, healthcare, gaming, and autonomous vehicles to gain traction.

However, given the scale of publicly traded (and the largest privately held) wireless tower and data center providers, it remains to be seen if edge deployments can move the revenue needle or impact the bottom line.